HD Hyundai Marine Solution IPO Valuation Analysis

Our base case valuation of HD Hyundai Marine Solution is target price of 98,254 won per share, representing an 18% upside from the high end of the IPO price range.

The company's ROE averaged 67% in 2022 and 2023. In comparison, the comps' ROE averaged 10.6% in the same period. [HD Hyundai Marine Solution > Comps]

Our base case valuation is based on 24.7x P/E (comps' average) using our estimated net profit of 178.7 billion won for the company in 2024.

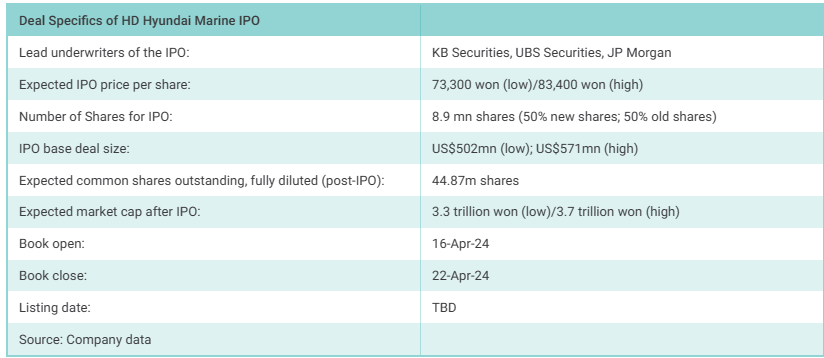

HD Hyundai Marine Solution is getting ready to complete its IPO in KOSPI in May 2024. This will be one of the largest IPOs in Korea in 2024. In fact, this is the largest IPO in Korea (in terms of IPO offered amount) since the listing of LG Energy Solution (373220 KS) in 2022.

The IPO price range is from 73,300 won to 83,400 won. The IPO offering amount is from 652.4 billion won to 742.3 billion won. According to the bankers' valuation, the expected market cap of the company is from 3.3 trillion won to 3.7 trillion won. The book building for this IPO will last from 16 to 22 April. The main underwriters for the listing are KB Securities, UBS, and JP Morgan.

The IPO offering involves 8.9 million shares. This involves HD Hyundai Marine Solution issuing 4.45 million new shares (50%) and 4.45 million shares out of 15.02 million shares held by second largest shareholder, Kolberg Kravis Roberts (KKR) as existing shares sale. HD Hyundai, the largest shareholder with 24.8 million shares, will not sell its shares in this IPO.

Use of IPO Proceeds - HD Hyundai Marine Solutions plans to use the funds from the IPO to strengthen its global network and research and development, solidify its market leading position in the Korean ship aftermarket service, expand its capacity for eco-friendly remodeling projects, and promote the advancement of ship digital business.

Company Background

Established in November 2016, HD Hyundai Marine Solution was established to respond to the increasing demand for aftermarket (AM) services for ships. The company's core business includes ships aftermarket services and eco-friendly remodeling and digital solutions for ships. HD Hyundai Marine Service has benefited from the improving cycle in the shipbuilding industry. The company also provides various ship parts including engine parts, exhaust value spindle, main bearing, fuel injection pump, and piston. It also provides various fluid machineries including thruster and propeller.

The company changed its name from HD Hyundai Global Service to HD Hyundai Marine Service in November 2023 to better reflect its focus on providing all solutions needed in the marine industry and commitment in leading an eco-friendly technology and digital transformation.

HD Hyundai Global Service Main Products/Services

HD Hyundai Marine Solution services (Source: Company data)

HD Hyundai Marine Solution Ship parts/services (Source: Company data)

HD Hyundai Marine Solution Bunkering Service (Source: Company data)

HD Hyundai Marine Solution Stationary Engine Power Plants (Source: Company data)

Eco-friendly remodeling of vessels subsidiary (Source: Company data)

Digital transformation with HMS: (Source: Company data)

Potential Inclusion in KOSPI 200

At the high end of the bankers' valuation assessment, HD Hyundai Marine Solution would have a market cap of 3.7 trillion won. Based on this figure, it would be the 101st largest stock in KOSPI. Therefore, HD Hyundai Marine Solution is likely to be included in the KOSPI 200 index in 4Q 2024, in our view.

How the Bankers Priced the IPO

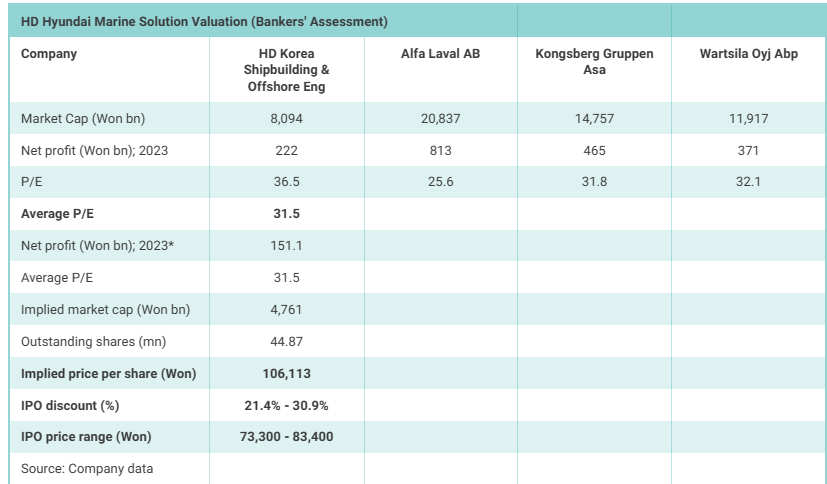

The bankers used four companies as comps including HD Korea Shipbuilding & Offshore Engineering, Alfa Laval AB, Kongsberg Gruppen Asa, and Wartsila Oyj Abp. The bankers then used their 2023 net profit and recent prices to derive average P/E of 31.5x.

The bankers then used HD Hyundai Marine Solutions' net profit in 2023 and applied the comp's average P/E of 31.5x to derive implied market cap of 4.8 trillion won or implied price of 106,113. After applying IPO discount range of 21.4% to 30.9%, this resulted in the IPO price range of 73,300 won to 83,400 won per share.

Income Statement Estimates

We estimate HD Hyundai Marine Solution (443060 KS) to generate sales of 1.6 trillion won (up 11.5% YoY), operating profit of 224.8 billion won (up 11.6% YoY), and net profit of 178.7 billion won (up 18.2% YoY) in 2024. Ships After Market Solution accounted for 42.4% of total sales in 2023, followed by Bunkering (41.4%), and Ecofriendly Ships Modeling (11.8%). We expect Ships After Market Solution to account for 45% of total sales in 2024, followed by Bunkering (39.6%), and Ecofriendly Ships Modeling (10.9%).

The company generated sales of 1.4 trillion won (up 7.2% YoY), operating profit of 201.5 billion won (up 41.9% YoY), and net profit of 151.1 billion won (up 44% YoY) in 2023. HD Hyundai Marine Solution's operating margin recently peaked at 15.5% in 2020 which declined to 10.6% in 2022 and increased again to 14.1% in 2023.

Source: Company data, Our Estimates

Source: Company data, Our Estimates

Sales Breakdown (By products/services) - The company breaks down its sales into four main units including Ships (After Market Solution), Bunkering, Eco-friendly ships remodeling, and others. Ships (After Market Solution), accounted by 42.4% of total sales in 2023, followed by Bunkering (41.4%), and Eco-friendly ships remodeling (11.8%).

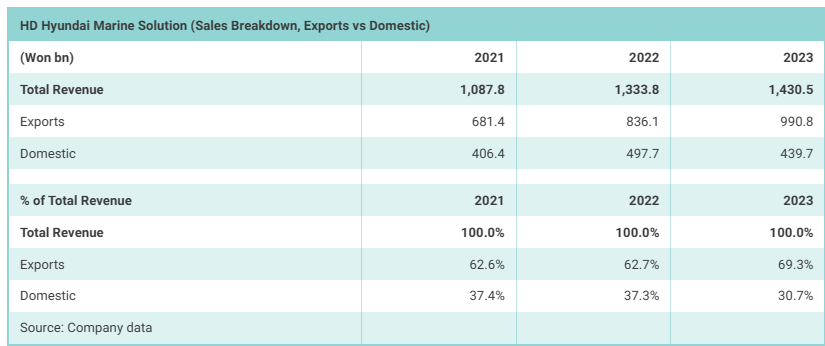

Sales Breakdown (Exports vs Domestic) - Exports accounted for 69.3% of total revenue in 2023, up from 62.7% of total revenue in 2022. Domestic sales accounted for 37.3% of total sales in 2022 and 30.7% of total sales in 2023.

Balance Sheet Analysis - The company has a moderately leveraged balance sheet. At the end of 2023, its debt ratio was 174% and current ratio was 154%. Its net debt to equity ratio was also 29% at the end of 2023.

Cash Flow Statement Analysis - The company generated positive cash flow from operations and free cash flow every year from 2019 to 2023. It had cash flow from operations of 72.9 billion won and free cash flow of 70.3 billion won in 2023.

Dividends - HD Hyundai Marine Solution paid out DPS of 2,000 won in 2022 and 2,500 won in 2023. Dividend payout ratio was 76% in 2022 and 66% in 2023. At the high end of the IPO price range (83,400 won) and assuming same DPS of 2,500 won in 2024 as in 2023, this would suggest a dividend yield of 3%.

Impact on HD Hyundai (267250 KS) & NAV Valuation

HD Hyundai (267250 KS) is the largest shareholder of HD Hyundai Marine Solution with a 62% stake. Mong-Joon Chung is the largest shareholder with a 26.6% stake in HD Hyundai. HD Hyundai also has treasury shares worth 10.5% of outstanding shares.

A successful IPO of HD Hyundai Marine would have a positive impact on HD Hyundai, which currently has a market cap of 5.4 trillion won. If HD Hyundai Marine Solution is valued at the high end of the bankers' valuation (3.7 trillion won), HD Hyundai's 62% stake in HD Hyundai Marine Solution would total 2.3 trillion won which would be 42% of HD Hyundai's current market cap. For further details, see our insight Asian Dividend Gems: HD Hyundai.

Our updated NAV valuation of HD Hyundai suggests implied base case price of 95,632 for HD Hyundai which is 40% higher than current price. The major components of value for HD Hyundai include its 73.9% stake in Hyundai Oilbank (estimated to be 7 trillion won), a 35.1% stake in HD Korea Shipbuilding & Offshore Engineering (009540 KS) (3.1 trillion won), a 37.2% stake in HD Hyundai Electric & Energy System (2.3 trillion won), and a 62% stake in HD Hyundai Marine Solution (2.3 trillion won).

For HD Hyundai Marine Solution, we used the bankers' high end valuation (3.7 trillion won) and applied HD Hyundai's 62% stake and applied additional 20% discount to derive a value of 2.3 trillion won. We also applied a 50% holdco discount on HD Hyundai.

Comparable Companies Valuation Analysis

Our base case valuation of HD Hyundai Marine Solution is implied market cap of 4.4 trillion won or target price of 98,254 won per share, which represents an upside of 18% from the high end of the IPO price range. Given the modest upside, we have a Positive View of this IPO. Our base case valuation is based on P/E of 24.7x our estimated net profit of 178.7 billion won for the company. Our base case valuation multiple of 24.7x P/E is based on the average P/E of the comps in 2024.

To value HD Hyundai Marine Solution, we used four comps including HD Korea Shipbuilding & Offshore Engineering (009540 KS), Alfa Laval AB (ALFA SS), Kongsberg Gruppen (KOG NO), and Wartsilia Oyj Abp.

Operating margin - The operating margin of the comps averaged 7.6% in 2022 and 2023. In comparison, HD Hyundai Marine Solution's operating margin averaged 12.4% in the same period. [HD Hyundai Marine Solution > Comps]

ROE - The company's ROE averaged 67% in 2022 and 2023. In comparison, the comps' ROE averaged 10.6% in the same period. [HD Hyundai Marine Solution > Comps]

Sales Growth - We estimate HD Hyundai Marine's sales to increased by 20% from 2022 to 2024. In comparison, the comps' are expected to experience average sales growth of 33% in the same period. [HD Hyundai Marine Solution < Comps]

Other Factors (Corporate Governance/Relationship with HD Hyundai Heavy Industries/Size Factor) - Other major factors including corporate governance and size factor weighs more negatively for HD Hyundai Marine Solution relative to the comps. However, its relationship with HD Hyundai Heavy Industries would be viewed positively. [HD Hyundai Marine Solution < Comps]

All in all, we are comfortable with using the comps' average P/E ratio of 24.7x in 2024 to value HD Hyundai Marine Solution which has higher ROE and operating margin than the comps but lower sales growth. In addition, HD Hyundai Marine Solution compares more negatively than the comps in terms of corporate governance and size factor.

Furthermore, in the first day of trading, unlike many smaller IPOs in Korea so far this year that have surged much higher, we do not expect a surging share price for HD Hyundai Marine Solution. Over the next 6-12 months, we believe a more likely scenario for the company is an upside of about 15% to 20% versus the IPO price.

Keep reading with a 7-day free trial

Subscribe to Douglas Research Insights to keep reading this post and get 7 days of free access to the full post archives.