ICTK IPO Valuation Analysis

Our base case valuation of ICTK is target price of 28,694 won, which is 79% higher than the high end of the IPO price range.

Our base case valuation is based on P/S multiple of 20.8x using our estimated sales of 18.1 billion won in 2025.

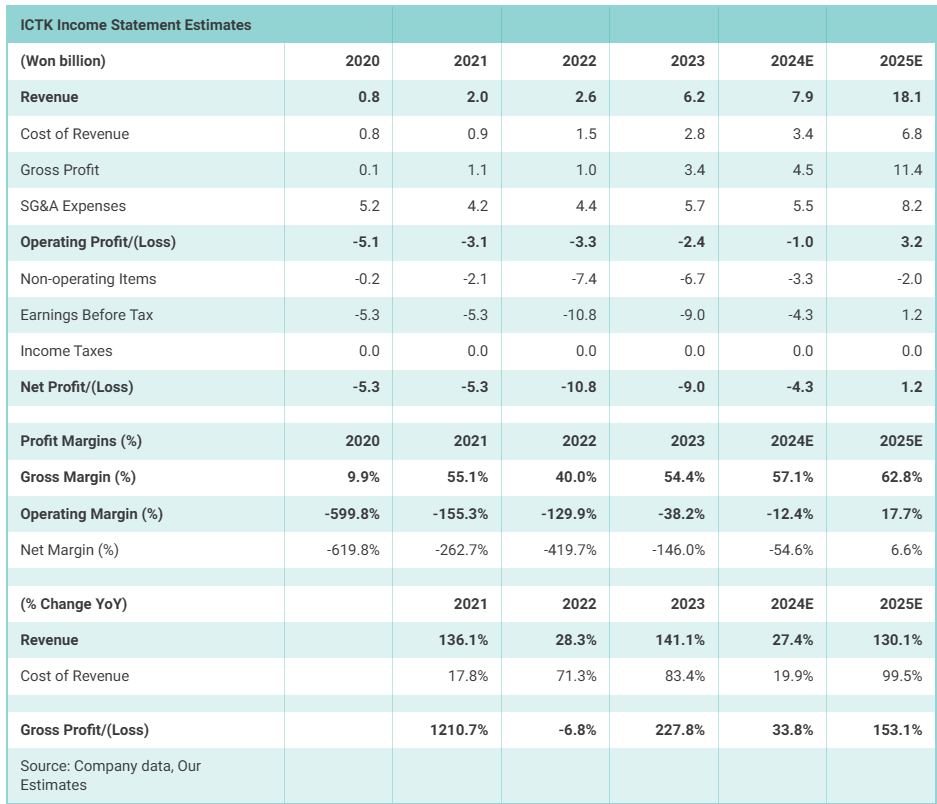

ICTK's operating margin improved from -129.9% in 2022 to -38.2% in 2023. We estimate its operating margin to improve further to -12.4% in 2024 and 17.7% in 2025.

Income Statement Estimates

We estimate ICTK to generate sales of 7.9 billion won (up 27.4% YoY) in 2024 and 18.1 billion won (up 130.1% YoY) in 2025. Our sales estimates are 5% lower than the company's Base Case A scenario in 2024 and 2025, respectively. We also estimate the company to generate an operating loss of 1 billion won in 2024 and an operating profit of 3.2 billion won in 2025. The company estimates an operating loss of 0.3 billion won in 2024 and an operating profit of 7.1 billion won in 2025. Therefore, our profit estimates are much more conservative than the company's estimates in the next two years.

The company's sales increased from 2.6 billion won in 2022 to 6.2 billion won in 2023. Its gross profit also jumped from 1 billion won in 2022 to 3.4 billion won in 2023. The company's gross margins improved from 40% in 2022 to 54.4% in 2023. We estimate the company's gross margins to improve further to 57.1% in 2024 and 62.8% in 2025.

Its operating margin improved from -129.9% in 2022 to -38.2% in 2023. We estimate its operating margin to improve further to -12.4% in 2024 and 17.7% in 2025. The improvement in the operating margin is driven by higher sales and lower SG&A as a percentage of sales. ICTK's SG&A as a percentage of sales declined from 169.9% in 2022 to 92.6% in 2023. We estimate SG&A as a percentage of sales to decline further to 69.4% in 2024 and 45.1% in 2025.

ICTK is getting ready to complete its IPO in KOSDAQ in May. The company plans to offer 1.97 million shares in this IPO. Total outstanding shares after the IPO is expected to be 13.13 million shares. The IPO price range is from 13,000 won to 16,000 won. The IPO offering is expected to raise from 25.6 billion won to 31.5 billion won.

According to the bankers' valuation, the expected market cap of the company after the listing is 171 billion won to 210 billion won. The book building for the institutional investors lasts from 24 to 30 April 2024. NH Investment & Securities is the lead underwriter of this IPO.

Major shareholder - Lee Jung-Won (founder) owns 15.3% stake in the company. Other related parties own an additional 17.6% stake in the company.

Lead underwriter providing a putback option on IPO investors - NH Investment & Securities, the lead banker on this deal, is providing a putback option in return for acquiring some shares of ICTK. This is rare for lead underwriters of IPOs in Korea and this is a strong testament of NH Investment & Securities' confidence in the company's technology and post IPO price performance. NH Investment & Securities has secured the right to acquire 98,500 shares of ICTK. At the high end of the IPO price range (16,000 won), this would amount to 1.6 billion won (US$1.2 million).

NH Investment & Securities decided to provide putback options to public offering investors while securing preemptive rights. The putback option refers to guaranteeing at least 90% of the public offering price to investors if the stock price falls based on the public offering price for up to 6 months from the day of listing.

Company Background

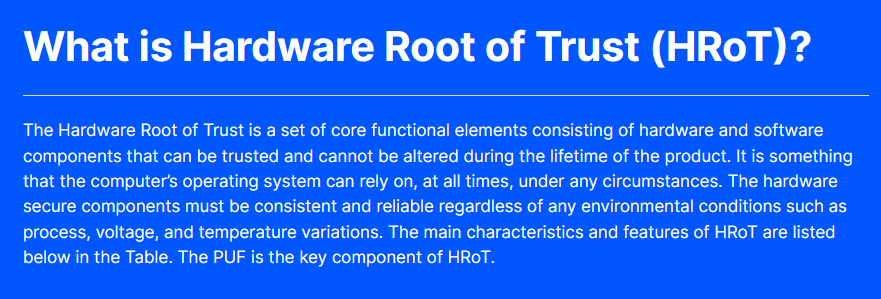

ICTK is a security company specializing in Internet of Things (IoT) based on physical copy prevention technology. ICTK has a unique technology called PUF which is a cutting-edge technology that creates a unique security key during the chip manufacturing process. This security key is very difficult to modify or duplicate.

PUF technology is recognized as one of the strongest means of protecting encryption keys. ICTK's VIA PUF technology utilizes the randomness that appears in the VIA Hole of the semiconductor wafer stage process. It is a concept based on semiconductor DNA, just as humans are born with biological IDs such as iris or fingerprints. In addition, ICTK is quickly preparing for the coming quantum computer era by launching a security chip equipped with a quantum tolerant algorithm (PQC).

All ICTK's products are based on PUF chips with strong security features. PUF chips can be molded into modules of the customer's choice.These chips and modules can be supported as a comprehensive security solutions and IP. It can be shaped and molded to be more user-friendly, but its security features are much stronger. Currently, the main module lineup includes Wi-Fi modules, LTE/5G modules, Secure UICC, and Secure USB/PCI modules. ICTK's security solutions are already in use in the market in across various fields such as user authentication, FOTA, KMS, PQC, and VPN.

The company has developed world's first e-SIM using PUF technology. The company has also successfully commercialized the PUF+PQC applied VPN solution and are preparing for CC certification (information security certification). ICTK is engaged in core technology (IP) sales and security chip, module device and platform businesses.

The company has enjoyed an excellent growth in sales in the past several years. Through a contract with a global big tech company, a full-scale supply is expected to begin next year. LG Uplus Corp (032640 KS) and Korea Electric Power (KEPCO) (015760 KS) are major current customers of the company.

What is PUF? (Source: Company data, Youtube)

Source: Company data

Source: Company data

Keep reading with a 7-day free trial

Subscribe to Douglas Research Insights to keep reading this post and get 7 days of free access to the full post archives.